Managing household finances

The reality is that no matter how big your salary is, expenses are bound to continue escalating if you do not find ways to keep them on a tight rein

Are you one of those people who is constantly whining about the size of your paycheck and pinning your hopes on salary increases to cope up with your household expenses and mounting debts? Chances are you are blaming your employer for the diminutive salary increases or the government for the increase in prices of commodities in the face of inflation.

People are quick to point the blame unto others for their wrong financial decisions.

The sad truth is that the majority of the Filipinos are overspending. It is common to hear employees lamenting that their salary could not last till the next payday. Oftentimes, they resort to borrowing cash from cooperatives, credit cards, or the friendly neighborhood lender in motorcycle to tide them over for the remaining days until their next payday.

They are so weighed down by their debts to the extent that even their job productivity and family relationships may have been affected.

The reality is that no matter how big your salary is, expenses are bound to continue escalating if you do not find ways to keep them on a tight rein. Even executives in large corporations can get in trouble. The executive compensation package with its corresponding perks allows them easier access to bank loans and obtain higher credit limit that enables them to acquire luxuries to keep up with a lifestyle perceived to be befitting of their status.

The reality is that no matter how big your salary is, expenses are bound to continue escalating if you do not find ways to keep them on a tight rein. Even executives in large corporations can get in trouble. The executive compensation package with its corresponding perks allows them easier access to bank loans and obtain higher credit limit that enables them to acquire luxuries to keep up with a lifestyle perceived to be befitting of their status.

If you can no longer find ways to increase your income, the most practical thing to do is to go over your expense items and adjust your lifestyle accordingly.

Perhaps it is high time for you to consider a paradigm shift. How about considering a different approach in handling your personal finance?

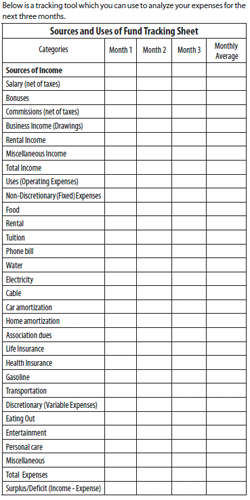

Household finance may be viewed as an ongoing business entity with its own sources and uses of fund.

Identify all sources of income and the operating expenses in maintaining the household. As you can see, the Operating Expenses maybe further classified into Non-Discretionary (Fixed) Expenses and Discretionary (variable) expenses. At the bottom of the tracker, you may get the difference between Total Income and Total Expenses to determine your surplus or deficit. The average column represents the average monthly figures for each expense item. So add the monthly figures for each expense item divide by three to get the monthly average. The categories are, by no means, exhaustive so you can add or delete certain items.

By using this tool, you can have a better grip of your cash flow and this consciousness will help you come up with a spending plan which will be the next step in the financial-planning process. A spending plan will help you prioritize expenses that matters to you based on your goals (short- ,medium- and long-term goals) and avoid impulse buying.

If you have not yet set up your emergency fund, this is where you can allocate a certain percentage of your surplus fund until you reach the desired amount. Please refer to previous article “Is your Emergency Fund Enough?”

At the outset, you may find it difficult to establish the habit of listing daily expenses as it entails discipline and will power on a daily basis to keep this habit in place. However, this simple commitment will go a long way in helping you to manage your financial affairs better. A paradigm shift augurs well in your journey toward financial wellness.

****

Arlyn Cheng is a Registered Financial Planner of RFP Philippines. She is a Financial Advisor of a leading insurance company in the Philippines.

Arlyn Cheng is a Registered Financial Planner of RFP Philippines. She is a Financial Advisor of a leading insurance company in the Philippines.

Source: http://www.businessmirror.com.ph/index.php/en/business/banking-finance/35099-managing-household-finances

Comments

3,386 total views, 1 views today

Social